Indirect Rates, Huh? What are They Good For?

With apologies to the 1970’s Motown hit, one of the most common questions we get at ReliAscent® surrounds development and utility of indirect cost rates....

With apologies to the 1970’s Motown hit, one of the most common questions we get at ReliAscent® surrounds development and utility of indirect cost rates....

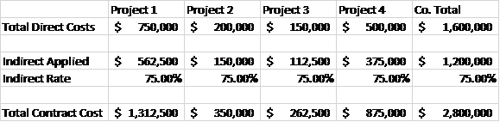

In a cost reimbursable job, we all know how the government will pay for direct labor and materials. In these awards, they also pay for a “fair share” of your overhead (or indirect costs). How does the...